Preserving wealth over the long term is not simply about choosing the highest-performing investments. It is about constructing a portfolio that can withstand economic shifts, market volatility and changing personal circumstances. Asset allocation – the strategic distribution of capital across different asset classes – plays a central role in achieving that balance. Rather than relying on individual stock selection or short-term market timing, experienced investors focus on diversification as the foundation of sustainable growth. Market commentators such as Kavan Choksi frequently highlight that consistent asset allocation decisions often have a greater impact on long-term results than isolated investment picks.

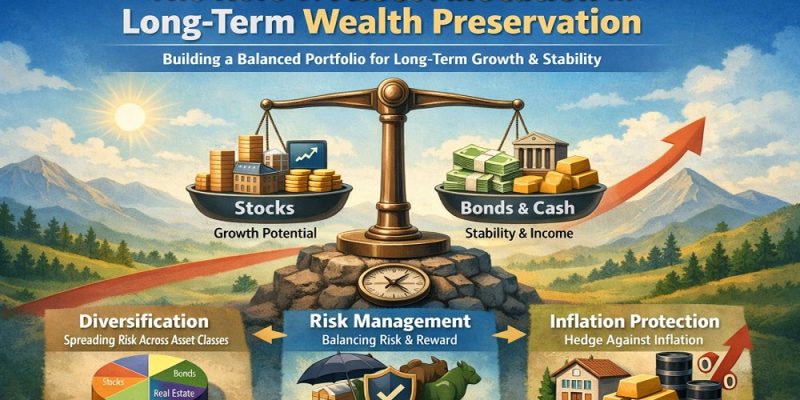

At its core, asset allocation is about managing risk. Different asset classes behave differently under varying economic conditions. Equities may offer strong growth during expansionary periods but can experience significant drawdowns during recessions. Bonds, on the other hand, often provide stability and income, particularly when interest rates decline. Real assets such as property or commodities may offer inflation protection, while cash preserves liquidity and flexibility. By blending these components thoughtfully, investors can reduce overall portfolio volatility without sacrificing long-term return potential.

One of the primary advantages of asset allocation is its ability to smooth performance across market cycles. When one asset class underperforms, another may offset losses. This dynamic does not eliminate risk entirely, but it helps mitigate the impact of severe downturns. For investors focused on wealth preservation – particularly those approaching retirement or managing intergenerational capital – controlling downside risk is often more important than maximising short-term gains.

Strategic allocation typically begins with defining clear objectives and risk tolerance. Younger investors with longer time horizons may accept greater equity exposure to capture growth. In contrast, those prioritising capital preservation may allocate a higher proportion to fixed income and defensive assets. The allocation mix should reflect not only market conditions but also personal financial goals, income requirements and liquidity needs.

Rebalancing is another essential element of effective allocation. Over time, market movements can cause certain assets to represent a larger share of the portfolio than originally intended. Periodic rebalancing restores the target mix, reinforcing discipline and preventing unintended concentration risk. This systematic approach also encourages investors to trim positions that have grown substantially and add to those that may be temporarily undervalued.

Inflation considerations further underscore the importance of thoughtful allocation. While cash may feel safe, it can lose purchasing power over extended periods of rising prices. Incorporating growth-oriented and real assets can help protect wealth in real terms. The key is balancing stability with the need to maintain long-term purchasing power.

In essence, asset allocation serves as the structural framework of a resilient investment portfolio. By diversifying across complementary asset classes, aligning strategy with personal objectives and maintaining disciplined rebalancing practices, investors can navigate uncertainty while preserving capital over time. It is this strategic consistency, rather than reactive decision-making, that supports enduring financial security.

Comments